Liberals have done a terrible job of pointing out how little conservative educational policy reformers understand about public education. Honestly, I think it is because few liberal journalists or politicians know anything about educational policy. They fall for the cheap tricks and rhetorical devices the conservatives trot out in fear that the right-wing wonks know something they do not. In general, that is not the case. Often, I would argue, they know less than nothing. They just lie to promote their narrative. Not only are they largely ignorant of the historical or current research on educational policy issues they almost universally seem to have no personal experience with public education. To the point that their work often reads like they just found out about some long-established piece of public education. “Can you believe that the government lets parents take out loans for their students? And apparently, it has been happening for decades!” Hell, they can barely be bothered to do any original research of their own at all. They just repeat other people’s work and tack on unsubstantiated conclusions and click-baity titles. A recent piece from George Leef in the National Review illustrates this point well.

Leef, the product of two private institutions for his BA and JD, wants you to know what a scam the Federal Parent Plus loan is. This insidious liberal government policy allows parents to take out loans to help cover their child’s cost of education. Leef cites the work of Preston Cooper, another privately educated man who’s only work in life seems to be suckling at the teat of the libertarian lobbying/think tank leviathan. Why do I describe it this way? Because Cooper works for so many think tanks concurrently that he’d need to be a superhuman who never sleeps in order to discreetly research and write for each of them. Oh, and like most “think tank intellectuals” he just copies other people’s work and adds some sloppy pre-canned opinion to their stats and calls it a day. This piece leverages the work of two Brookings Institute researchers with no discernable research or substantiated insight provided by Cooper. It is essentially a game of telephone, from Brookings to Cooper at the James Martin Center to Leef at the National Review. Top notch work there, conservative think tank echo chamber.

Cooper would have readers believe that the loan program is uncapped. That is highly misleading. There is no lifetime cap, as there is for individual student loans, but there are annual caps based on total annual cost of the college their child is enrolled at minus other financial aid (i.e., aid the student takes out in their own name, grants, and/or scholarships). Since the loans are tacked to cost, the only way the parent loans would be huge would be the student taking no loans. What is the frequency of this? And should non-wealthy parents not have that option? He also wants you to call these high-interest loans. They are 7% loans. For wealthy people with good credit, this may seem high, but this is a pretty low figure in the experience of everyday American’s interactions with our finance system. And would be far higher for most borrowers in a private program. In fact, the Federal student aid site and any financial aid officer at a college will tell you that if you or your parents have great credit a private loan might be a better option. Why do you think the private market cannot beat the government market for these loans? Because the Federal profits are lower than the private industry would accept for “riskier” candidates. He also claims that there are basically no credit checks. Again, this is false. The threshold for the amount of delinquent debt is fairly low (under $3000) and the credit standards are high enough that this loan program which is not designed to be profitable IS. Cooper also has the audacity to state that while the program literally makes money for the Federal government it “is not hard to imagine” that someday it might not. Sure. He does not tell you when that is likely to happen or under what circumstances. Instead, he simply asks you to imagine it.

Now that Cooper has made an imaginary problem—a “predatory lending scheme that loses the Federal government money”—he proposes a solution. Push more student loan debt onto students using private lending.

Go look at Preston Cooper’s work. You will find that he often proposes this as the solution. Everything he writes starts with the answer “private industry should handle this (and make money off it)” and then searches out a problem (real or imagined) to apply it to.

Cooper closes by saying there was never a good reason for the Federal government to lend to parents in the first place. Remember, only wealthy people should be allowed to help their children pursue the American Dream!

In Leef’s retelling of Cooper’s reimagining, this boils down to Parent PLUS loans are predatory loans designed to fail:

Additionally, there is a predatory aspect to Parent PLUS lending, since the government allows people to borrow even though it has already determined through the education department, in its analysis of financial need, that the family has no ability to help support a college student.

When you play the game of conservative intellectual telephone you end up with ever more bizarrely false statements. Just as the earnings of students may increase over time, so too can the earnings of working- and middle-class parents. This may come as a shock to the upper class, but regular Americans tend to have kids fairly young. Like when they are still in their early 20s. They often send their kids off to school while they are entering their prime earning years—their forties and early fifties. My dad was 43 and my mom was 41 when I moved off to college. Their earnings increased a lot since that time period (and they are both still two presidential election cycles away from retiring!). Mom had an associate’s degree and dad a high school education. Hardly the profile of people who should be helping their son go off to college. I was certainly deemed eligible to take out full loans while my parents also took out PLUS loans. My parents were upper middle class by earned income, but based on the costs of college and their dependents at home would not have been able to afford to pay my tuition AT THE TIME. Instead, we split the bill using Federal loans. This is how and why the parent loans are calculated the way they are. It is not based on whether or not you could pay instalments of this amount over the next decade. After all, the schools themselves are not offering you a line of credit. It is based on the question of “do the parents currently have the assets to pay for college costs out of pocket”? How many non-wealthy American families can?

Without liquidating your retirement and getting a second mortgage that figure is basically zero (and that is ignoring that the majority of American families with college-aged children have no such retirement fund and likely no paid off property to leverage).

Conservative higher education finance policy reformers want two things. They want access to your money that currently goes to the government to provide such wide access to higher education. And they want to limit how many non-elite children are competing with their kids on the academic and job market.

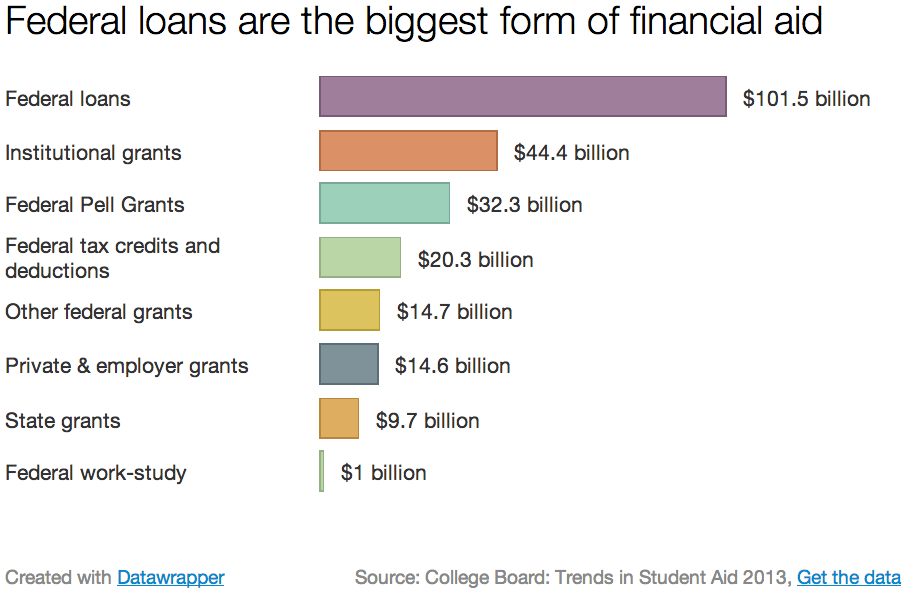

Do not forget that these are the same lobbyists who pushed for the systematic defunding of public education that has foisted loans on students and parents in the first place. First, they said that the state shouldn’t be paying for higher education– people should have to take out loans for it. Indeed, loans are far and away the largest form of financial aid.

Now they want to make sure that the government is not providing lower cost loan options to students and their families to even do that. Only rich people deserve the luxury of helping their kids pay for college. And if your son or daughter cannot handle a larger debt load at a higher interest rate to pursue a degree then maybe they should go do something more “practical.” These folks fundamentally oppose a society where merit is given any consideration in favor of one where the deck is stacked in favor of the rich and connected. Options for the rich. Hard reality for the poor and middle class.

You tell me which side of this debate is hostile to the everyday American, responsible for the shrinking middle class, or killing our ability to pursue the American Dream?

The Parent PLUS program has been a huge success at what it set out to do—provide greater access to higher education for students who have the ability but lack the means to afford to attend competitive higher education institutions (thereby enriching themselves in both mind and pocketbook) in an environment of declining public funding. I’d be happy to dismantle it and replace it with a more stabilizing and just system of higher education financing—say through federal and state taxes, the way they used to be. Killing options that provide reasonably priced options to people in need in favor of a deregulated private lending sector that has a long history of truly predatory behavior? That is a total non-starter.